Recent years have seen tremendous growth for ridesharing services such as Uber and Lyft in New York, both in New York City and in Upstate. For many car owners, Uber and Lyft offer an excellent way to make money on a schedule that works for them and the demand for drivers is currently very high. If you’re interested in driving for a rideshare company, or you already do, you should know that auto insurance works a little differently in your situation.

Your personal vehicle insurance policy does not cover transporting passengers for a fee. Both Uber and Lyft offer insurance for their drivers, but there are significant limitations to that coverage that you should be aware of, and perhaps purchasing extra insurance may be in your best interest.

What does my personal insurance cover?

Personal Driving

Your automobile insurance is designed to protect you (and others) financially in the event of an accident with the understanding that you are driving your vehicle to commute to work, to run errands, or for leisure. In other words, driving for personal reasons.

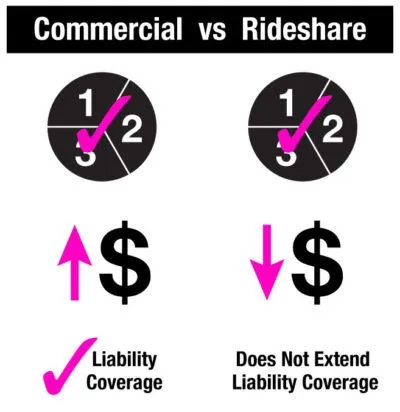

But when you drive your vehicle for the purpose of making money transporting passengers, your insurance considers that driving to be commercial driving. Thus, if you are involved in an accident during such a use, your personal auto insurance will not cover you. The reason your insurance coverage ends when you drive your vehicle as part of a business is that the risks are much greater than when you’re driving it for your personal use. This risk increases the likelihood that your insurer will have to pay out on a claim and insurance companies stay profitable by paying out as little as possible for each claim.

Commercial Driving

To drive for Uber or Lyft in New York State, you must maintain the state’s minimum insurance coverage on your vehicle. If you drive an Uber or Lyft in New York City, however, you are required to have commercial auto insurance (described below) as mandated by the New York City Taxi and Limousine Commission (TLC), in addition to other important requirements from Uber and Lyft.

What type of coverage do I get through Uber or Lyft?

It’s helpful to think of how insurance coverage works as an Uber or Lyft driver if you think of the time you’ll spend driving in three phases:

Phase 1

You are driving your car with the Uber or Lyft app turned OFF.

Phase 2

You are driving your car with the Uber or Lyft app turned ON, but you have not yet received a request for a ride from a passenger.

Phase 3

You are driving your car, the Uber or Lyft app is turned ON, and you have received a passenger request and are either on the way to pick them up or you are actively driving them to their destination.

In Phase 1, only your personal insurance policy is covering you.

In Phase 2, Uber and Lyft provide minimal insurance coverage only if you don’t have your own coverage, and because you are driving for commercial purposes, your personal insurance policy won’t cover you in the event of an accident.

Uber and Lyft provide the following minimum coverages:

- $75,000 for the driver’s liability for bodily injury per person,

- $150,000 per covered accident for bodily injury,

- $25,000 per accident for property damage for which the rideshare driver is responsible,

- $25,000 Uninsured/Underinsured Motorist Protection,

- Personal Injury Protection (PIP), also known as “No-Fault” Insurance, which is required by state law. ($50,000 per accident Upstate/$200,000 in New York City).

In Phase 3, Uber and Lyft both provide substantial insurance coverage, as required by law, for you, your passengers, and others.

- $1,250,000.00 for bodily injuries to you, your passengers, pedestrians, people in other vehicles, and property,

- $1,250,000.00 bodily injury coverage for you and your passengers against uninsured/underinsured motorists, and

- If you have comprehensive & collision coverage already on your vehicle, extra coverage up to the value of your vehicle, with a $2,500.00 deductible.

In summary, the type of insurance coverage you have while driving for Uber or Lyft depends very much on whether you are in Phase 1, Phase 2, or Phase 3, described above.

During Phase 2, there may be a significant gap in your insurance coverage.

When you are driving for Uber or Lyft with the app turned ON, but you haven’t yet received a passenger request, your insurance coverage is not nearly as robust as when you’ve received a request or when you are transporting passengers. Your personal insurance will not cover you during this time because you are engaged in commercial driving.

While Uber and Lyft offer some coverage during this type of driving, it’s not much higher, if at all, than the state’s minimum insurance requirements. You may find yourself paying out of pocket after an accident, especially if you’re injured.

Furthermore, there is no collision coverage provided by Uber or Lyft during Phase 2. Therefore, any damage to your vehicle during this time will have to be paid out of pocket by you. Even in Phase 3, where you receive supplemental collision insurance, the $2,500.00 deductible may be too much for you to afford, and the coverage is only a supplement if you already have collision coverage for your vehicle.

You will also not be eligible for your personal insurance company’s emergency roadside assistance or rental car reimbursement during Phase 2 or 3 if these are part of your policy.

What type of insurance should I have as an Uber/Lyft Driver?

Ideally, to cover the gap in insurance coverage outlined above, you would want to get a commercial auto insurance policy. This type of insurance offers the most complete protection for you if you drive for a rideshare company. It effectively covers you during all stages of driving and is required if you drive for either Uber or Lyft within New York City.

However, not everyone can afford a commercial auto insurance policy outside of New York City and it may not make financial sense even if you can. This is particularly true if your income from rideshare driving is relatively small, such as if you only drive for the rideshare company on weekends, holidays, and/or for special events such as concerts and festivals.

A better option may be rideshare insurance, sometimes called “gap insurance coverage.” Rideshare insurance offers the best of both worlds. It is a blend of both personal and commercial auto insurance, offering more inclusive coverage than that offered by Uber or Lyft yet costing much less than commercial auto insurance. It extends your personal policy’s benefits to Phase 2 of driving for a rideshare company, giving you enhanced medical coverage, emergency roadside assistance and rental car reimbursement, should you already receive this coverage. Plus, if your insurance’s collision deductible is lower than the $2,500.00 offered by Uber and Lyft, with rideshare insurance you would only have to pay the lower amount after an accident during Phase 3 that damaged your car.

Rideshare insurance typically extends all the coverage of your personal insurance policy to your ridesharing activities in Phase 2. With the exception of liability coverage, this is also true during Phase 3 of rideshare driving. With rideshare insurance, if you have a claim, or a passenger is injured and files a claim against you, you would be able to communicate directly with your insurance company rather than through Uber or Lyft for your insurance needs.

While not offered everywhere and by every insurance company, rideshare insurance is becoming more popular due to customer demand. The key, as always, is to shop around to get the best rate. If your current insurer doesn’t offer rideshare insurance, be sure to speak to someone and ask them to make such policies available. Insurance companies do listen to their customers and hope to keep them as future customers.

Conclusion

If you are considering becoming a rideshare driver, or you already are one, take a look at your current policy. Unless you have a commercial auto insurance policy, you likely do not have the coverage you need for all the situations you’ll be encountering.

Contact your current insurer first to see if they offer rideshare insurance or gap insurance to cover you when you’re “on duty” but not currently carrying passengers or on your way to a pickup. It will be much less expensive than a commercial insurance policy while ensuring that you are ideally protected in the event of an accident. If your current insurer does not offer this type of insurance, check with the rideshare company/companies you either drive for or are interested in driving for. They may be able to point you to insurers in New York that offer rideshare insurance. Be sure to do an Internet search as well, so you can shop around for the best rate possible.

Also, be aware that the rideshare landscape is still new enough to be changeable and rapidly evolving. Stay up to date on current developments in your area, as well as nationally, so that your rideshare driving experience is both rewarding and safe.

Driving for a rideshare company can be a lucrative sideline or primary source of income for many, but be sure you’re financially protected in the event of an accident so you can quickly get back on the road and earning.

Rideshare Insurance Videos

Contact an Attorney

If you or anyone you know has been injured in an Uber or Lyft rideshare accident, or an automobile accident of any kind, the attorneys at Harding & Mazzotti, LLP have a wealth of experience in dealing with insurance companies and in protecting your rights to receive the compensation you deserve. Our attorneys handle all types of motor vehicle accidents, including those involving automobiles, motorcycles, and all types of truck accidents, from eighteen-wheelers to delivery vans.

Contact us today for a free case evaluation by calling 1-800-LAW-1010 (1-844-722-3596). We’re here 24 hours a day, 7 days a week to take your call, or use our convenient online contact form here.